China's steel prices forecast next week: Inventories will recover from fluctuations in steel prices

2019-02-22 12:13:09

Affected by the inertia of the traditional festivals, the market price of the main steel products market has increased sharply after slight fluctuations. At present, the support for steel prices continues to weaken, but with the fall in crude steel production and the recovery of downstream demand for steel, the pressure between supply and demand has been further improved, but the rapid rise in steel stocks will also bring short-term repression. The short-term domestic steel is expected. The market will maintain a slight fluctuation adjustment.

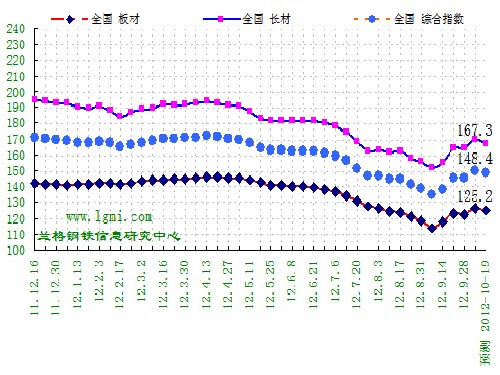

Affected by the inertia of the traditional festivals, the market price of the main steel products market has increased sharply after slight fluctuations. At present, the support for steel prices continues to weaken, but with the fall in crude steel production and the recovery of downstream demand for steel, the pressure between supply and demand has been further improved, but the rapid rise in steel stocks will also bring short-term repression. The short-term domestic steel is expected. The market will maintain a slight fluctuation adjustment. According to the Lange Steel Information Research Center weekly price forecast model data, this week (2012.10.15-10.19) the domestic steel market price will fluctuate slightly, long products market will be slightly adjusted, and the plate market price will rise and fall. The Lange Steel Composite Index is expected to fluctuate around 148.4 points, with an average correction of around 1.5 points. The average steel price is around 3860 yuan, with an average volatility of around 30-50 yuan. Lange Steel's long product index is expected to fluctuate around 167.3. The callback is about 2.2 points; Lange Steel's price index for sheet metal is expected to fluctuate around 125.2 points, with a correction of about 1.1 points.

From the market research of the Lange Steel Information Research Center, it is expected that the domestic long product market prices will be slightly adjusted this week (2012.10.15-10.19), while the plate market prices will rise and fall; raw material market prices will vary. The market prices of iron ore and billet will remain basically stable, scrap market prices will be significantly adjusted back to 100 yuan, and coke market prices will rise by 20 yuan.

1. The domestic steel market increased sharply this week. Week 41 of 2012 (10.8-10.12) The Lange Steel (LGMI) Composite Price Index reached 149.9 points, a 3.00% increase on a week-on-week basis and a decrease of 18.33% from the same period of last year. Among them, the LGMI long product price index was 169.5 points, a week-on-month increase of 2.99%, a decrease of 18.38% over the same period last year; LGMI sheet price index was 126.3 points, a week-on-month increase of 3.02%, a decrease of 18.26% over the same period last year (see Figure 1 for details) .

According to the price data of 17 categories of 44 standard varieties monitored by the Lange Steel Information Research Center market, the price of major steel products in the 41st week of 2012 (10.8-10.12) has sharply increased. Compared with last week, the prices have increased. With a sharp increase, the flat variety has decreased, and the falling variety has decreased significantly. Of these, 38 varieties rose, 21 more than last week; 4 were flat, down 7 from the previous week; 2 varieties fell, down 14 from the previous week. The price of domestic steel raw materials market has risen sharply, coke market prices have risen steadily by 50 yuan, scrap market prices have risen sharply by 150-200 yuan, iron ore market prices have risen by 30-40 yuan, and billet market prices have risen by 180 yuan.

2. This week, the country's steel stocks have been reduced from a downward trend. At present, the nation's steel inventories have risen from a downward trend to a higher level, with building materials and sheet stocks all decreasing. According to the market monitoring of Lange Steel Information Research Center, on October 12th, the national steel society inventory was 13.4984 million tons, an increase of 494,700 tons from the previous week. From the perspective of sub-species: China's wire rod social inventory is 1,169,900 tons, up 14.79% from last week; rebar, social inventories are 5,460,000 tons, up 4.28% from last week; Panluo social inventory is 318,900 tons, This was an increase of 1.64% from last week; the social volume of hot-rolled coils was 3.8923 million tons, up by 1.46% from last week; the social volume of CRC coils was 1,605,800 tons, up by 0.46% from last week; the plate's social inventory The amount was 1.655 million tons, up 3.48% from the previous week.

3. Steel market turbulence heightened this week. In the 41st week of 2012 (10.8-10.12), the market of rebars fluctuates. However, in the upward process, the thread also showed some negative things, and the rise was gradually weak. Weekly settlement price rose by 42 points this week, continuing the upward trend after the week before the holiday, but the gains have narrowed, and the rapid release of power gradually signs of failure. This week, the main contract was 1.01 million contracts, an increase of 135,000 hands, and the position returned to the top of 1 million hands again. It can be seen that the funds don't cool down on the thread clusters. The gradual enlargement of the positions will once again brewing the medium-level market.

4. Concern about the recent factors affecting steel prices Macroeconomics:

In September, China's manufacturing PMI was 49.8%, the first rise since May. On October 1, the China Manufacturing PMI released in September by the China Federation of Logistics and Purchasing and the National Bureau of Statistics Service Survey was 49.8%, compared to the previous month. It rose 0.6%, and the index has risen since May of this year. Among the main sub-indexes, only a few indices have dropped slightly. Most of the indices have rebounded to different degrees. In particular, the major leading index such as the new order index and raw material inventory index rebounded significantly. The effect of policy measures indicating stable growth of the country gradually emerged, and the economic operation gradually Stabilizing the bottom has laid a good foundation for steady economic growth in the fourth quarter. From the 11 sub-indexes, only the finished goods inventory index, the employees index, the supplier delivery time index decreased slightly, and the other indices all rebounded in varying degrees. In terms of different industries, 8 industries including agricultural and non-staple food processing industry, textile and apparel industry, food and wine beverage refined tea manufacturing industry, and ** product industry are higher than 50%; electrical machinery equipment manufacturing, general equipment manufacturing, non- Thirteen industries, including metal mineral products, ferrous metal smelting and rolling processing, and textiles, are less than 50%.

China's HSBC manufacturing PMI rebounded slightly in September HSBC (September 29) announced that China’s September HSBC Manufacturing Purchasing Managers’ Index (PMI) was revised up to 47.9 from the 41 hits in August. The lowest level since the month. The initial value of HSBC Manufacturing PMI for China in September was 47.8, and the final value in August was 47.6. Due to weaker demand from China's major trading partners, the sub-index for new export orders fell to 44.9 in September, the lowest level in 42 months. In September, the input price and output price index for the fifth consecutive month fell below 50, but both rose slightly from the previous month. The monthly employment index was below the watershed for seven consecutive months, but it has rebounded from the previous month. Nearly 85% of the interviewed companies stated that the employment level is basically unchanged.

The NDRC has intensively approved 15 overseas investment projects and energy projects account for half of the total. According to the National Development and Reform Commission's official website, the National Development and Reform Commission has approved 15 overseas investment projects in a centralized manner, marking a new high since the beginning of this year, involving energy, finance, telecommunications, and infrastructure, among which energy projects have Seven, including three solar photovoltaic projects, one nickel mine project, one oil company acquisition project, and the other two are transmission lines and power projects. In addition, there are **, rubber, infrastructure, cargo ships, tires, and telecommunications projects, respectively, and there are two other types of industrial equity acquisition projects.

Raw material supply:

Conditions for Admittance of Scrap Iron and Steel Processing Industry announced The Ministry of Industry and Information Technology announced on October 11 the “Entry Requirements for Scrap Iron and Steel Processing Industry†to set clear requirements on the layout, construction, technology, scale, equipment, and product quality of scrap steel processing enterprises.

The “access conditions†have comprehensively increased the access threshold for the scrap processing industry. Its requirements: The newly-built scrap steel processing and distribution enterprise must have an annual scrap steel processing capacity of 150,000 tons or more; by the end of 2014, the annual capacity of scrap steel processing for the transformation and expansion of waste steel processing and distribution companies should reach more than 100,000 tons. The new scrap steel processing and distribution company requires that the factory area is not less than 30,000 square meters, the land use procedures are legal (the lease contract is not less than 15 years), and the operation site is not less than 15,000 square meters. The reconstruction and expansion of scrap steel processing and distribution companies requires that the factory area is not less than 20,000 square meters, the land use procedures are legal (the lease contract is not less than 15 years), and the operation site is not less than 10,000 square meters. The integrated power consumption of the processing and production system for newly-built and expanded waste steel processing and distribution companies should be less than 30 kWh/ton of scrap steel, and the new water consumption should be less than 0.2 tons/ton of waste steel.

The “admission requirements†also require that natural reserves, scenic spots, drinking water source protection areas, basic farmland protection areas, and other areas that require special protection shall be determined by national laws, regulations, rules, and plans or by the people’s governments at or above the county level. Within the area, within one kilometer of the residents' gathering area and other enterprises that strictly prevent pollution, no new steel scrap processing and distribution enterprises shall be built. The scrap steel processing and distribution companies that have been put into operation in the above-mentioned areas must gradually withdraw in accordance with the requirements of the regional plan and, within a certain period of time, pass laws, such as relocation or conversion.

Industry News:

In September, Tongye PMI 53.2% entered the expansion zone. On October 1, the Lange Steel Information Research Center released September 2012 PMI for steel, which was 53.2%, which rose by 7.6 percentage points from the previous month and entered expansion. The interval shows that the steel market has further improved. Judging from the prior relationship between Tongyue PMI and steel prices, the short-term market will improve and steel prices will continue to rise. From the sub-indexes, the 10 sub-indexes in September showed a different degree of recovery from the previous month, of which five entered the expansion range, and five are still in the contraction range. Among the major sub-indicators, the sales volume index, total order index, and purchase willingness index continue to rise and enter the expansion range; the inventory index, environmental index, and trend judgment index are still in the contraction range. The data for September showed that by the end of October, demand in the Chinese steel market had further improved, the contradiction between supply and demand for steel products had eased, and the confidence of steel companies had improved. The steel prices in the latter period are expected to continue to rise. As the steel market still faces the situation that the main demand has not been released and the environment is tense, the steel price continued to rise in October and there is still a downside risk.

In the second half of September, the average daily output of crude steel decreased by 0.74% month-on-month

According to statistics from the China Iron and Steel Association, the average daily output of crude steel for major and medium-sized enterprises in the second half of September 2012 was 1.509 million tons, down by 0.9% from the previous month; the average daily crude steel output in the country in late September was estimated at 1.842 million tons. Decline by 0.74% from the previous month.

According to statistics from the China Iron and Steel Association, 80 steel companies accounted for profits in August. From January to August, the accumulated sales revenue of key large and medium-sized steel companies that were included in the statistics of the Association of Steel and Steel was 2,368.609 billion yuan, 6.21% lower than the same period of last year. 4.312 billion yuan, 66.8% lower than the same period of last year, total profit -3.184 billion yuan, down 104.22% year-on-year. Among them, August sales revenue was 279.45 billion yuan, profits and taxes were 95 million yuan, profit income was -4.196 billion yuan, and profitability fell to the lowest point of the year. Among the 80 large and medium-sized iron and steel enterprises included in the statistics of the Steel Association, the number of loss-making enterprises in August was more than half, reaching 44. In the month of August, the key large- and medium-sized steel companies that were included in the statistics of the Association of Steel Associations reported a profit margin of -1.5%, while the accumulated sales margin for January to August was -0.13%.

According to statistics from Hebei Metallurgical Industry Association, from January to August, the cumulative profits of 64 (total 68) key steel companies in Hebei Province have accelerated to decline year-on-year. Accumulated profits in August reached 1.798 billion yuan, 88.41% lower than 15.504 billion yuan in the same period of last year. The total profit for the month plummeted from a loss of 114 million yuan in July to a loss of 1.632 billion yuan in August. Among them, from January to July, the iron and steel industry in Hebei Province achieved a profit of 8.167 billion yuan, a year-on-year decrease of 52.75%, and the profit rate dropped to 1.19%. Although it is higher than the national average, it is still in a very low state. According to the data released by Hebei Province, the current steelmaking capacity in Hebei is 286 million tons. As such, the crude steel production in Hebei in the first half of this year was 939.696 million tons, and the capacity utilization rate was only 65.7%, which was in a state of serious overcapacity.

The previous session of the thread ** closed down on the 12th, the main contract fell 0.11%

The rebar main 1301 contract was opened at RMB 3,638/ton in the morning on the 12th, and then the price showed an intraday volatility and downtrend throughout the day. The lowest was RMB 3,616/ton throughout the day and RMB 3,671/ton was highest, closing at RMB 3,638/ton. On the previous trading day (11th), the settlement price fell by 4 yuan/ton, 1,924,836 contracts, 1,010,092 positions, 53,074 contracts.

Downstream demand:

China will continue to develop high-speed rails with a total length of 18,000 kilometers. The “Twelfth Five-Year Plan for Comprehensive Transportation System†newly issued by the State Council proposes that China will establish a “four vertical and four horizontal†high-speed rail network in 2015, and build related assistance. Lines, extension lines, and tie lines. According to the Ministry of Railways, the total mileage of China's high-speed rail will reach 18,000 kilometers by then. High-speed railway refers to railways that travel at a speed of over 200 kilometers per hour. At present, China's high-speed rail operating mileage is 6,894 kilometers. The "planning" also mentioned that at that time, the national rapid rail network will be basically established. More than 40,000 kilometers of express railway lines with speeds over 160 kilometers per hour will reach more than 40,000 kilometers, more than the end of the “Eleventh Five-Year Plan†(2006-2010), basically covering more than 500,000 population cities.

From January to August, China's total output value of the internal combustion engine industry was 110.232 billion yuan. According to statistics, in August of this year, the year-on-year growth rate of the industrial output value and industrial sales value of the internal combustion engine industry of China's internal combustion engine declined slightly compared with the previous month, and the export delivery value was the same The growth rate has increased significantly. At the same time, the sequential growth rate of the total industrial output value and industrial sales value all increased significantly from the previous month, and turned from negative growth to positive growth. The chain-to-month growth rate of export delivery values ​​also rose from the previous month. From January to August, the total output value of China's internal combustion engine industry was 110.232 billion yuan, a year-on-year increase of -2.36%; the accumulated sales value was 110.002 billion yuan, an increase of -1.82% year-on-year; from January to August, the industry cumulative sales ratio was 99.79%. The industry achieved an export delivery value of 7.714 billion yuan, a cumulative year-on-year growth rate of 14.94%. The country produced a total of 1001.2925 million kilowatts of engines, with an accumulative growth rate of 2.01% over the same period of the previous year. Among them, the output of auto engines was 8.4879.52 million kilowatts, which fell from 8.07% in the previous month to 7.65%.

Railway infrastructure investment increased by 111% year-on-year in September

According to the statistics of the Ministry of Railway Statistics Center, domestic railway fixed asset investment reached 72.658 billion yuan in September, a year-on-year increase of 92.7%, an increase of 52.7%; and infrastructure investment was 64.277 billion yuan, a year-on-year increase of 111% and an increase of 63.8%. From January to September 2012, domestic railway fixed asset investment reached 344.156 billion yuan, a 13% decrease from the same period in 2011; of which railway infrastructure investment was 290.251 billion yuan, a decrease of 54.828 billion yuan compared with the same period of last year.

According to statistics from the China Association of Automobile Manufacturers, the overall performance of automobile production and sales in September was not satisfactory. The cumulative growth rate fell for the first time after eight consecutive months of increase, and was once again below the level of the same period of last year. In the same month, the production and sales volume of automobiles reached 1.609 million units and 1.167 million units, up 10.6% and 8.2% respectively from the previous month, and production increased by 3.7% over the same period of last year. Sales decreased by 1.8% from the same period of last year. From January to September, the production and sales of autos were 14,013,200 vehicles and 14,092,300 vehicles, an increase of 5% and 3.4% respectively from the same period of the previous year. The growth rate was 0.2 and 0.7 percentage points lower than that in the first eight months respectively.

Material :Natural slate , quartz,sandstone ,marble etc .

Size :12''*12''

Shape :Square shape

Packing :Hard carton then fumigated strong wooden crate.

The wooden crate size is made as the container size . After loading the wooden crate in the container ,the wooden crates will nearly same size with the width of the container .It can make the wooden crate not have space to move during transport . In this case ,it can keep the stone safety mostly

Application : Can be used to decorate the outside wall or inside wall .Decorate your house ,decorate your life .

Marble Mosaic,Marble Mosaic Tile,Marble Mosaic Floor Tile,Stone Mosaic Tile

HEBEI DFL STONE , http://www.dflstone.com